Divvy Homes offers a new school approach to an old school option for home ownership

Say the words “rent to own” and someone might shoot you an uneasy look or even worse, start talking about predatory lending practices.

It’s true that many of the well-documented risks are legitimate and the initial home owner — often a corporation — has leverage over the renter, but the marketplace is evolving. Several new players are adding some creative and consumer-friendly wrinkles that make rent-to-own a more palatable option, especially for prospective buyers who are working on building their credit scores or cannot afford a traditional down payment on a home.

One of those disruptors in the market that has come to Central Florida and Polk County is Divvy, a property focused technology startup that says its mission is to “make home ownership accessible to everyone.”

On the company’s website, divvyhomes.com, there are nearly two dozen homes available in Polk County where renters can start leasing to lock in a purchase price on the home that is based on current and projected market conditions, as well as how soon the buyer purchases the home. A renter has up to three years to purchase the home at the contracted price.

The company is based out of San Francisco and has a valuation of more than $2 billion dollars despite being less than five years old.

It has been profiled by the “New York Times”, is mentioned frequently in articles about more people warming up to more unconventional routes to home ownership , and it was even recently named one of the best workplaces in the Bay Area by “Fortune Magazine.”

What follows is quick education on the Divvy model, some insights from industry experts of rent-to-own and an interview with Tom Egan, CFO at Divvy Homes, with a special interest to Central Florida home buyers in particular.

How Does the Divvy Rent-to-Own Model Work?

- Y

ou locate a home in Divvy’s inventory that you would like to purchase, whichcontractually has to be done within three years

ou locate a home in Divvy’s inventory that you would like to purchase, whichcontractually has to be done within three years - You make a one-time, upfront payment (1 to 2 percent of your home’s value) that goes straight toward savings for your future down payment

- As part of your monthly payment, 5 to 25 percent of those funds go into a “savings” that will be applied to your home purchase price if/when you qualify for a mortgage and decide to purchase it

- Divvy is responsible for all major repairs to the homes they own, and tenants agree to work closely with them to schedule those repairs in a timely and agreed upon manner; the maintenance costs are built-in to the monthly payments

- If you decide to purchase the home, it is based upon the agreed upon price for purchasing it either before 18 months of renting or before and up to 36 months of renting; if you choose to not purchase the home or cannot qualify for a mortgage you must provide a 60-day notice; you will retain the “savings” funds you have put in on a monthly basis and will be charged a re-listing fee

ou locate a home in Divvy’s inventory that you would like to purchase, whichcontractually has to be done within three years

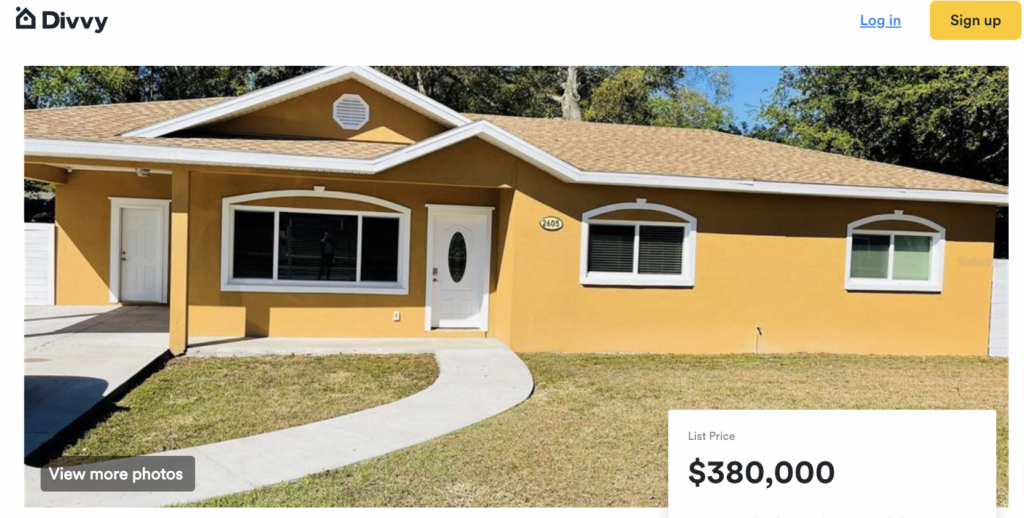

ou locate a home in Divvy’s inventory that you would like to purchase, whichcontractually has to be done within three yearsExample of an Actual Divvy Homes listing

2605 S. Lincoln Ave.  3 bedroom, 2 bath

3 bedroom, 2 bath

Listed price: $380,000

Monthly payments: $2,810 w/5 percent going into home savings account, $3,405 w/10 percent going into home savings account

Buyback price before 18 months: $417,193

Buyback price before 36 months: $454,385

What Financial Experts Are Saying About Rent-to-Own

PROS

- You don’t have to wait to build up a down payment to lock in the home you want, and you don’t have to qualify for a mortgage right away1

- It allows potential homeowners to pay down debt while putting money toward a “down payment” concurrently2

- You can avoid buyer competition, and everything is negotiable1

- It provides a tenant the opportunity to get in a home they love with time to build their credit3

CONS

- Rent is almost always more expensive on a monthly basis than a mortgage for the same house1

- You often lose money if you decide not to purchase the house1

- If the owner defaults on the home while you are in a rent-to-own agreement you could be forced to leave2

- Locking in a purchase price far in advance of qualifying for a mortgage is a roll of the dice because of often changing market conditions3

Q&A With Divvy Homes CFO Tom Egan

Tom Egan, Divvy Homes CFO

RJ asks….

What is the primary challenge or problem Divvy aims to solve in today’s home market?

Tom answers…

What we set out to do was really create a pathway from renting into owning that was reflective of sort of the way society had moved and the way incomes had changed and the way home ownership had changed. Where we started was the most acute pain point, which was that exact transition from renting to owning; the reality is most people, especially people that are buying a home for the first time, don’t know what it means to get a mortgage, don’t know what title insurance is or what an escrow agent doe, or what a down payment is or what a mortgage is supposed to look like.

You combine all of that with the fact that, again, asset prices keep running away, and it’s really, really difficult, if not impossible, for somebody — especially a first time home buyer — or somebody that doesn’t come from more of an ownership background.

RJ asks…

With the rent-to-own category as a whole having a less than glowing reputation, how do you ease someone’s fears about considering an updated, more robust model of it?

Tom answers…

It’s funny, when I first interviewed to join Divvy, I spoke with a board member, an investor at the time…who funny enough, was calling me from the back of an Uber. He was on his way to or from the airport. And I asked a similar question, because again, rent-to-own is not a product, you know, that has a great history. And he said, ‘…everybody always told their kid don’t get in the back of a car with somebody that you don’t know who’s offering you candy. And now we all do it every day. We get in the back of an Uber or in the back of a Lyft. And it’s not because suddenly you just weren’t cynical or skeptical about it anymore, but it’s in many cases, it’s just that you gotta figure out how to cross that trust chasm. So you have to do it yourself and you have to earn that trust for us. It is very much earned.

RJ asks…

One argument against the rent-to-own model is very few renters actually become homeowners of the property. What does the data on renting to ownership currently look like at Divvy?

Tom answers…

It’s about 50 percent conversion, to exercise the option. We obviously want to do better than that, but we’re very proud of that number, because it’s, as far as we’re aware, 8-10 times what the next closest competitor does. The data is a little bit difficult to coerce, but the other businesses that are out there — I think going back to the point around philosophy — the other businesses that are out there I think in some ways are not quite as transparent.

And frankly, at the end of the day, their goal is not to necessarily get the customer to buy the home, but instead to build a portfolio of assets, right? The way I like to think about it is, we’re only owning the asset in service of the customer’s experience. We’re not buying assets because we wanna own assets long term, we’re buying assets because that’s what we need to do in order to service the customer’s experience.

RJ asks…

Divvy is currently in 19 major metro markets and six of them in Florida. Why does Divvy have such an interest in Florida?

Tom answers…

The demographics suit our product really well. It’s a lot of young families, a lot of millennials that are just in the household formation years.

It’s growing in the right direction. The economy’s growing very strongly in Florida. We also look at, you know, how levered is the local economy to a single employer or a single industry. Florida’s pretty diverse in that regard. There’s a diverse population of people. There’s a diverse population of businesses. It’s not like hyper levered to oil and gas or hyper levered to entertainment or something that is, excuse me, cyclical.

The housing quality housing stock is good, good quality. We develop local relationships with brokerages, with construction companies, folks on the ground. At the end of the day, like we’re operating from California, but we need to make sure that we’ve got local relationships because fundamentally, you know, real estate is local. Like you can’t pick up the house and move it; you can’t turn a house into a crypto coin.

RJ asks…

Why is Divvy making a more concentrated effort to get into the regions outside of major metro areas, specifically a city like Lakeland?

Tom answers….

We generally tend to operate in that first and second ring of suburbs… and that target zone has expanded as more and more people have gone fully remote. At the end of the day, it’s gotten awfully expensive and a lot of people are having to go further out to find space that is compatible with their budget.

[Lakeland] is a bit outside the area traditionally considered ‘metro Tampa or Orlando,’ but if you look in, like Atlanta, for example, the population has sprawled quite a bit. It’s a very large city and people are moving an hour and a half, an hour and 45 minutes outside of the city because that’s where they wanna be in terms of space and that’s where they can afford to be with. And it’s very interesting, you see like the price for square foot drops by 20, 30, 40, 50 percent when you go another 10 miles. And you’re like, that seems like a good trade

Sources:

1 – Ramsey Solutions

2 – Bankrate.com

3 – Experian